In today's dynamic financial landscape, finding a secure and rewarding place for your savings is more crucial than ever. Money Market Accounts (MMAs) stand out as an excellent option, offering a compelling blend of competitive interest rates, liquidity, and the security of federal insurance. For many, MMAs strike the perfect balance between a traditional savings account and a checking account, allowing easy access to funds while growing your money at a healthier rate than conventional savings options. This comprehensive guide will delve into what makes an MMA a top choice, how to identify the best accounts, and what factors to consider to maximize your savings potential in 2026.

What Exactly is a Money Market Account?

A Money Market Account (MMA) is a type of savings account offered by banks and credit unions that typically pays a higher interest rate than a regular savings account. They offer features similar to checking accounts, such as check-writing privileges and debit card access, making your funds readily available when needed. However, it's essential to understand that MMAs are distinct from another financial product with a similar name: Money Market Funds.

Money Market Accounts vs. Money Market Funds: Understanding the Key Differences

While their names are similar, Money Market Accounts and Money Market Funds serve different purposes and carry different levels of risk. A **Money Market Account (MMA)** is a deposit account offered by banks and credit unions. It is insured by the Federal Deposit Insurance Corporation (FDIC) for banks, or the National Credit Union Administration (NCUA) for credit unions, up to $250,000 per depositor, per insured institution, for each account ownership category. This federal insurance provides a critical layer of safety, making MMAs a very low-risk savings option.

In contrast, a **Money Market Fund (MMF)** is a type of mutual fund. These are investment products, not bank deposit accounts. Money market funds invest in highly liquid, short-term debt securities, such as U.S. Treasury bills, certificates of deposit (CDs), and commercial paper. While generally considered low-risk investments, they are *not* FDIC or NCUA insured. This means that, unlike MMAs, the principal in an MMF is not guaranteed against loss, although the risk of losing money is historically very low. Understanding this distinction is paramount for risk-averse savers looking for guaranteed principal protection.

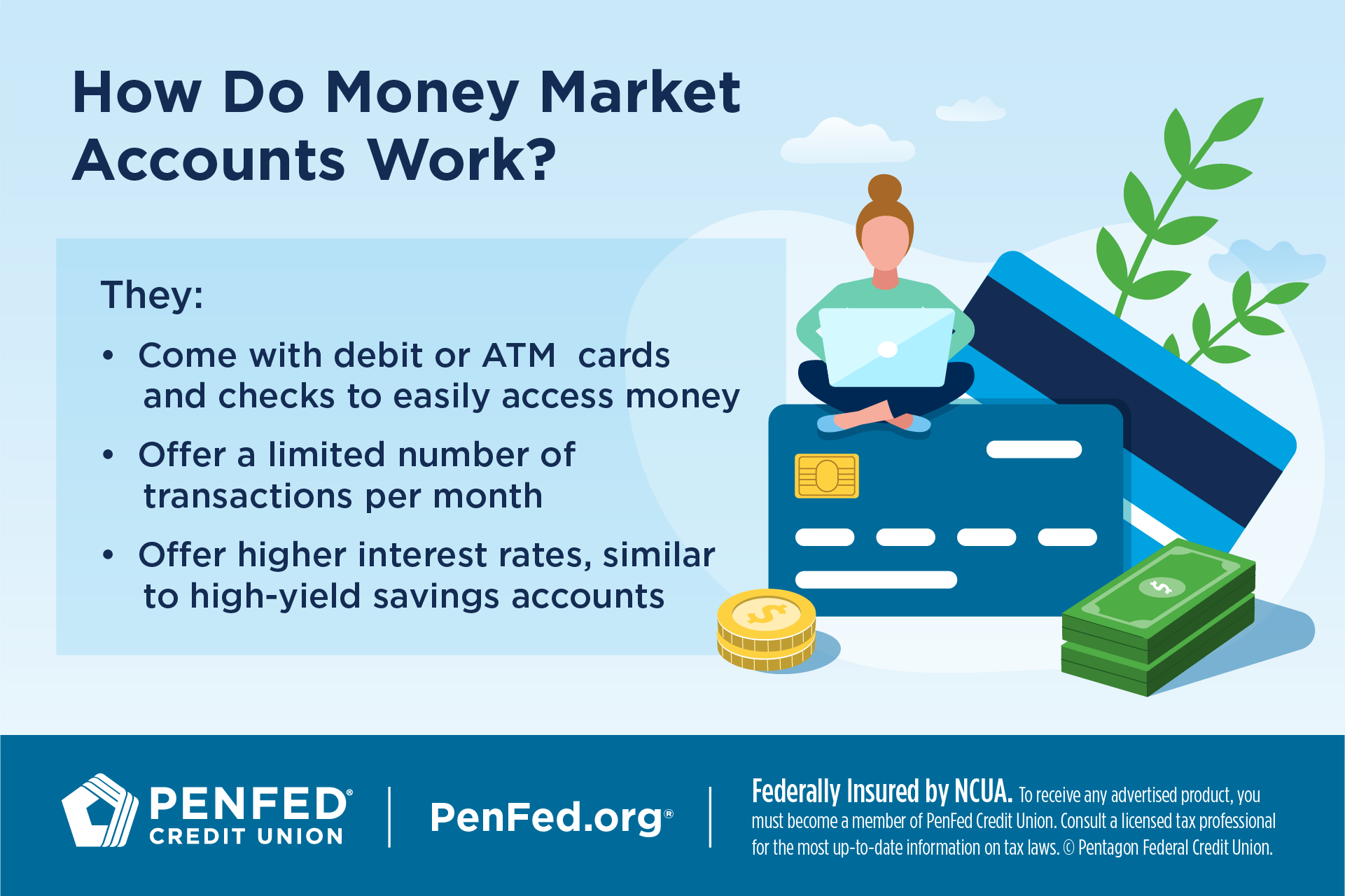

How Money Market Accounts Work

Money market accounts offer a unique combination of features. They typically come with variable interest rates, meaning the Annual Percentage Yield (APY) can fluctuate based on market conditions, often tracking the federal funds rate. This can be advantageous in a rising interest rate environment. Unlike regular savings accounts, MMAs often provide check-writing capabilities, a debit card for transactions, and easy electronic transfers. However, they are subject to federal transaction limits under Regulation D, which generally restricts certain outgoing transfers and withdrawals to six per statement cycle. Exceeding this limit can result in fees or even conversion of the account to a checking account.

Why Choose a Money Market Account?

Choosing the right savings vehicle is a personal decision, but money market accounts offer several compelling advantages that make them attractive for many savers.

Competitive Interest Rates

One of the primary draws of money market accounts is their potential to offer higher interest rates compared to traditional savings accounts. In environments where the Federal Reserve raises interest rates, MMA rates often follow suit, providing a better return on your deposited funds. It's common to see top-tier MMAs offering APYs in the range of 3.50% to 4.50% or even higher, significantly outperforming the national average for standard savings accounts. This competitive yield allows your money to grow more effectively over time.

Liquidity and Accessibility

Money market accounts provide an excellent balance between earning interest and maintaining easy access to your money. Unlike Certificates of Deposit (CDs), which lock up your funds for a specific term, MMAs allow you to withdraw money as needed, usually through various convenient methods. This liquidity is a major advantage for emergency funds or for money you might need access to in the short term, without sacrificing earning potential. Access methods typically include debit cards, checks, online transfers, and ATM withdrawals.

FDIC Insurance Protection

The safety of your principal is a critical concern for any savings account. Money market accounts offered by FDIC-insured banks (or NCUA-insured credit unions) provide robust protection. Your deposits are insured up to $250,000 per depositor, per institution, for each account ownership category. This means that even if the bank were to fail, your money would be protected up to these limits, offering peace of mind that your hard-earned savings are secure.

Key Factors When Comparing Best Money Market Accounts

To find the best money market account for your needs, it's important to evaluate several key features beyond just the advertised interest rate.

Annual Percentage Yield (APY)

The Annual Percentage Yield (APY) is arguably the most crucial factor. It represents the actual annual rate of return, taking into account the effect of compounding interest. Always compare APYs when evaluating different MMAs, and look for accounts that consistently offer rates significantly above the national average. Be aware that APYs can be variable and may change with market conditions, so understanding the bank's history of offering competitive rates is also beneficial.

Minimum Balance Requirements

Many money market accounts come with minimum balance requirements. Some might require a substantial initial deposit to open the account or maintain a certain average daily balance to earn the highest APY or to avoid monthly service fees. Assess whether these minimums are achievable for you. Some online banks may offer MMAs with no minimum balance or much lower thresholds, making them more accessible.

Fees and Charges

Unnecessary fees can quickly erode your earnings. Be diligent in reviewing the fee schedule for any money market account you consider. Common fees include monthly service fees (often waived if you meet certain balance or activity requirements), excess transaction fees (for exceeding Regulation D limits), ATM fees, and wire transfer fees. Look for accounts with transparent fee structures and reasonable ways to avoid charges.

Access to Funds (Transaction Limits)

While MMAs offer more flexibility than CDs, they are still subject to federal limits under Regulation D, which restricts certain outgoing transactions (like transfers to other accounts or third-party payments) to six per statement cycle. Some banks may also impose their own additional limits on ATM withdrawals or debit card transactions. Ensure the account's transaction limits align with how frequently you anticipate needing to access your funds.

Online and Mobile Banking Features

In today's digital age, convenient online and mobile banking platforms are essential. Look for MMAs that offer robust features such as easy fund transfers, mobile check deposit, bill pay, account alerts, and clear statements. A user-friendly digital experience can greatly enhance your ability to manage your money market account efficiently.

Top Picks for Best Money Market Accounts in 2026

As of 2026, the market continues to offer a variety of strong money market account options. While specific rates are highly variable and change frequently, certain types of institutions consistently rank high for competitive offerings.

High-Yield Online Money Market Accounts

Online-only banks and digital-first financial institutions often lead the pack in offering the highest APYs. This is largely due to their lower overhead costs compared to traditional brick-and-mortar banks. These accounts typically feature rates around 4.00% APY or sometimes even higher, making them excellent choices for maximizing returns. Examples often include popular online banks known for their competitive savings products. These accounts are ideal for individuals comfortable managing their finances digitally and who prioritize yield over in-person branch access.

Money Market Accounts with Low Minimums

For savers who may not have a large sum to deposit initially, several institutions offer money market accounts with low or no minimum balance requirements. While the APY might be slightly lower than those with high minimums, these accounts provide an accessible entry point to earn better interest than a standard savings account. These are often found at smaller community banks, credit unions, or specific online platforms designed for broader accessibility.

Money Market Accounts with Branch Access

While online accounts often boast the highest rates, some individuals prefer the option of in-person banking. Traditional banks and credit unions with physical branches offer money market accounts that provide this convenience. The trade-off, however, is that their APYs might not be as competitive as those from online-only institutions due to higher operating costs. For those who value face-to-face service or need to deposit cash frequently, these accounts can still be a good fit, provided their rates are respectable.

How to Open a Money Market Account

Opening a money market account is a straightforward process, typically taking only a few minutes once you have your information ready. This practical guide will walk you through the steps.

Step-by-Step Guide

1. Gather Required Documents: Before you begin, have your personal identification ready. This usually includes a government-issued ID (like a driver's license or passport), your Social Security Number (SSN), and your current residential address. You might also need information for funding the account, such as your existing bank account details for an electronic transfer.

2. Choose the Right Bank or Credit Union: Based on your research into APYs, minimum balances, fees, and accessibility preferences (online vs. branch), select the financial institution that best meets your needs. Look for institutions with a strong reputation and positive customer reviews.

3. Apply Online or In-Person: Most banks offer online applications, which are quick and convenient. You'll fill out a form with your personal and financial details. If you prefer, or if the bank requires it, you can visit a local branch to complete the application with a banking representative.

4. Fund Your Account: Once your application is approved, you'll need to make an initial deposit. This can typically be done via electronic transfer from another bank account, mailing a check, or making a deposit at a branch. Be sure to meet any minimum initial deposit requirements to activate the account and potentially secure the best rates.

5. Set Up Online Access and Features: After funding, set up your online banking portal, mobile app access, and any desired features like bill pay or direct deposit. Order checks or a debit card if these features are offered and useful to you.

What to Expect After Opening

Once your money market account is open and funded, you can start enjoying its benefits. Regularly monitor your account's APY, as it is variable and can change. Keep an eye on your balance to ensure you meet any minimums required to avoid fees or earn preferred rates. Make use of the convenient access methods for your transactions while staying mindful of federal (and any bank-specific) transaction limits to prevent penalties. Most banks provide detailed statements (electronic or paper) that outline your interest earnings and transactions.

Money Market Accounts in the Current Economic Climate: Rates and Inflation

Understanding how money market accounts perform within the broader economic context, particularly concerning interest rates and inflation, is key to making informed financial decisions.

Understanding Current APY Trends

Money market account Annual Percentage Yields (APYs) are closely tied to the Federal Reserve's monetary policy, specifically the federal funds rate. When the Fed raises rates, banks generally increase the rates they offer on deposit products like MMAs to attract funds. Conversely, when the Fed cuts rates, MMA yields tend to decrease. In 2026, many financial experts anticipate that rates will remain competitive, potentially even seeing some slight fluctuations. This makes MMAs a favorable option for capital preservation and moderate growth compared to lower-yielding alternatives.

Protecting Your Savings Against Inflation

While money market accounts offer competitive interest rates, it's crucial to consider them in the context of inflation. Inflation erodes the purchasing power of money over time. For your savings to truly grow, the APY you earn on your money market account should ideally be higher than the current rate of inflation. If inflation outpaces your MMA's APY, your real return (after accounting for inflation) will be negative, meaning your money can buy less in the future. Therefore, when evaluating the "best" money market account, always compare its APY not just to other accounts, but also to the prevailing inflation rate to ensure your savings are genuinely working for you.