In today's dynamic financial landscape, finding a secure yet rewarding place for your savings is paramount. High yield money market accounts have emerged as a compelling option for many individuals looking to maximize their returns without taking on excessive risk. These accounts blend the accessibility of a savings account with interest rates that often surpass traditional savings offerings, making them a popular choice for emergency funds, short-term savings goals, and everyday cash management.

/AFCU_70-HYSA-MoneyMarket-2d-padd.png?width=1500&height=1091&name=AFCU_70-HYSA-MoneyMarket-2d-padd.png)

What Exactly is a High Yield Money Market Account?

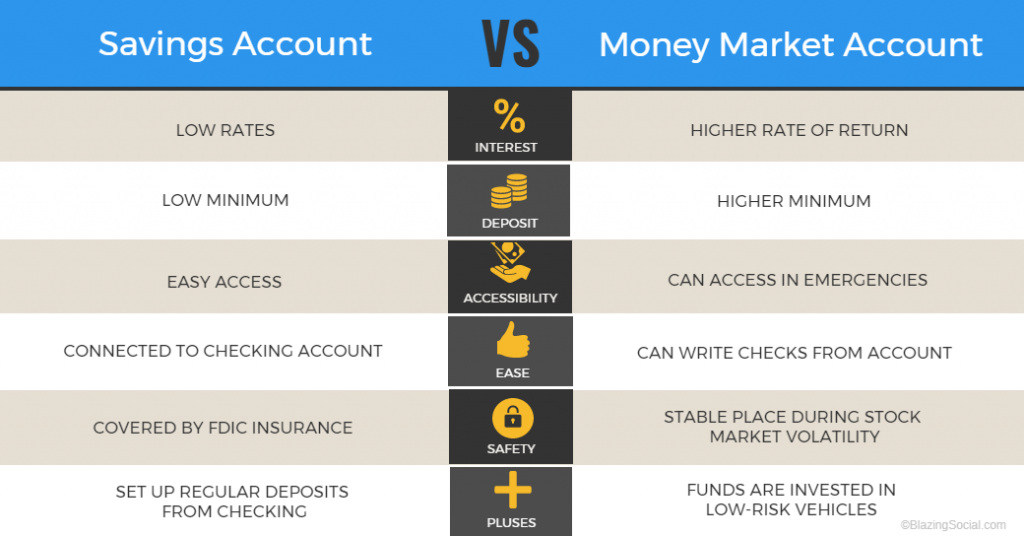

A high yield money market account is a type of savings account offered by banks and credit unions that typically pays a higher interest rate than a standard savings account. Unlike money market funds, which are investment vehicles (mutual funds) that invest in short-term debt securities, money market accounts are deposit accounts. This distinction is crucial because deposit accounts, when offered by FDIC-insured banks or NCUA-insured credit unions, provide federal insurance up to the standard limits ($250,000 per depositor, per institution, per ownership category). This insurance offers a significant layer of security, protecting your principal in the event of a bank failure.

While they offer higher yields, high yield money market accounts also come with some features commonly associated with checking accounts, such as limited check-writing privileges or a debit card for easy access to funds. However, these transactional features usually come with restrictions, such as a limit on the number of outgoing transactions (e.g., six per statement cycle) as per federal regulations (Regulation D), although this regulation has seen some relaxation recently. The primary purpose remains saving, not frequent spending.

Key Characteristics of High Yield Money Market Accounts

- Higher Interest Rates: Generally offer more competitive Annual Percentage Yields (APYs) compared to traditional savings accounts.

- Liquidity: Provide relatively easy access to funds through checks, debit cards, or electronic transfers, though typically with transaction limits.

- Safety: FDIC or NCUA insurance protects your deposits up to federal limits, making them a very low-risk option.

- Minimum Balance Requirements: Some high yield money market accounts may require a higher minimum deposit to open or maintain the account to earn the advertised high yield.

High Yield Money Market Accounts vs. High Yield Savings Accounts: What's the Difference?

The terms "high yield money market account" and "high yield savings account" are often used interchangeably, and indeed, they share many similarities. Both aim to offer better interest rates than conventional savings accounts and are typically FDIC or NCUA insured. However, there are subtle differences:

High Yield Savings Accounts

High yield savings accounts are straightforward savings vehicles. Their primary function is to store money and earn interest. They generally do not offer check-writing capabilities or debit cards, focusing purely on savings. They are an excellent choice if your main goal is to grow your emergency fund or save for a specific goal without needing frequent access to the funds via checks or cards.

High Yield Money Market Accounts

As mentioned, money market accounts often provide limited transactional features like check-writing or a debit card. This can be a minor convenience for some users who occasionally need direct access to their savings beyond electronic transfers. In practice, the interest rates offered by high yield money market accounts and high yield savings accounts can be very similar, and the "best" option often comes down to the specific rates and features offered by individual institutions at any given time, as well as your personal banking habits. For instance, in March 2026, many top money market accounts were offering APYs around 4.00% to 4.41%, similar to leading high-yield savings accounts.

Understanding High Yield Money Market Rates and How They Work

The interest rates on high yield money market accounts are variable, meaning they can change over time based on market conditions and the broader economic environment, especially the federal funds rate set by the Federal Reserve. When the Fed raises rates, money market account rates often follow suit, and vice-versa. This variability is why it's important to keep an eye on "high yield money market rates today" or "best money market account rates" to ensure your money is earning as much as possible.

Banks offer these competitive rates to attract deposits, which they then use for lending and other investments. The yield is typically expressed as an Annual Percentage Yield (APY), which takes into account the effect of compounding interest. A higher APY means more money earned on your deposit over a year.

Factors Influencing Money Market Account Rates:

- Federal Funds Rate: The target rate set by the Federal Reserve heavily influences short-term interest rates, including those for money market accounts.

- Inflation: Banks often adjust rates to keep pace with inflation, ensuring real returns for depositors.

- Competition: The competitive landscape among banks and credit unions plays a significant role. Institutions offering the "best money market accounts" are often those aggressively competing for deposits.

- Economic Outlook: General economic health and forecasts can impact a bank's willingness to offer higher rates.

Who Should Consider a High Yield Money Market Account?

High yield money market accounts are ideal for individuals and families who:

- Want Higher Returns on Liquid Savings: If your emergency fund or short-term savings are sitting in a low-interest checking or traditional savings account, a high yield money market account can significantly boost your earnings without locking up your funds.

- Prioritize Safety and FDIC Insurance: For those who are risk-averse, the federal insurance provides peace of mind that their principal is protected.

- Need Occasional Access to Funds: The limited check-writing or debit card features can be a convenient hybrid for managing funds that need to be accessible, but not for daily transactions.

- Are Saving for Specific Short-Term Goals: Whether it's a down payment on a car, a vacation, or a large purchase in the near future, these accounts can help your money grow faster than in a regular savings account.

How to Find the Best High Yield Money Market Accounts

Finding the right high yield money market account involves comparing several factors beyond just the APY:

1. Compare Interest Rates (APY)

This is often the most significant factor. Look for institutions consistently offering some of the "highest yield money market rates." Be aware that some rates may be promotional and revert after a certain period.

2. Check Minimum Balance Requirements

Some accounts require a minimum balance to open or to earn the highest APY. Ensure you can meet these requirements to avoid fees or lower interest rates. Many online banks offer excellent rates with little to no minimum balance.

3. Understand Fees

Investigate any monthly maintenance fees, excess transaction fees, or other charges that could eat into your earnings. Often, these fees can be waived by maintaining a certain balance or meeting other criteria.

4. Review Accessibility and Transaction Limits

While money market accounts generally offer more transactional flexibility than high-yield savings, confirm the specific limits (e.g., number of free withdrawals, check-writing availability) to ensure they align with your needs.

5. Verify FDIC/NCUA Insurance

Always confirm that the bank or credit union is insured by the FDIC (for banks) or NCUA (for credit unions) to protect your deposits. Most reputable institutions will prominently display this information.

6. Read Reviews and Customer Service Quality

Consider the bank's reputation for customer service. Online reviews can offer insights into other customers' experiences regarding account management, support, and ease of use.

Can You Lose Money in a Money Market Account?

This is a common and important question. For high yield money market *accounts* (deposit accounts), the risk of losing your principal is extremely low due to federal insurance. As long as your account is at an FDIC-insured bank or NCUA-insured credit union and your total deposits at that institution are within the insurance limits, your money is protected. The only "loss" you might experience is if the interest rate falls below the inflation rate, meaning your purchasing power slightly corrodes over time, but your nominal principal amount remains intact and continues to earn interest.

This contrasts with money market *funds* (mutual funds), which, while generally low-risk, are not FDIC insured and can, in rare circumstances, "break the buck" (meaning their net asset value falls below $1 per share), leading to a loss of principal. It's crucial to understand this distinction when evaluating your options.

Conclusion

High yield money market accounts offer an attractive solution for savers seeking a blend of competitive returns, liquidity, and security. By understanding their features, comparing them with high-yield savings accounts, and carefully researching the best available rates and terms, you can make an informed decision to optimize your cash management strategy. These accounts remain a robust tool for building emergency savings and achieving short-term financial goals in a relatively stable and rewarding environment. For businesses looking to optimize their cash, consider exploring why your business needs a money market account.