:max_bytes(150000):strip_icc()/are-money-market-accounts-considered-checking-or-savings.asp-final-cdfb86cadd614436badd72168a285667.png)

In the dynamic world of business, effective cash management is paramount to sustained growth and operational stability. While traditional checking and savings accounts serve their basic functions, a Business Money Market Account (BMMA) offers a sophisticated solution for businesses looking to optimize their cash reserves. Bridging the gap between liquidity and competitive returns, a BMMA can be a strategic asset for companies of all sizes. This comprehensive guide will delve into what a business money market account is, how it works, its key benefits, comparisons with other financial products, and crucial factors to consider when choosing the right one for your enterprise.

What Exactly is a Business Money Market Account?

A Business Money Market Account is a type of savings account offered by banks and credit unions, specifically designed for businesses. It shares characteristics with both a traditional savings account and a checking account. Like a savings account, it typically earns a higher interest rate than a standard business checking account. However, it also provides limited transactional capabilities, similar to a checking account, allowing businesses a degree of flexibility in accessing their funds.

The primary appeal of a BMMA lies in its hybrid nature: it allows businesses to keep their operational cash reserves readily accessible while simultaneously earning a more attractive yield than a non-interest-bearing checking account or even a low-yield business savings account. These accounts are ideal for storing emergency funds, accumulating capital for upcoming projects, or holding surplus cash that isn't immediately needed but might be required on short notice.

Key Features and Benefits for Your Business

For businesses striving for financial efficiency, a Business Money Market Account presents several compelling advantages:

Higher Interest Rates on Idle Cash

One of the most significant benefits of a BMMA is its potential to generate higher interest rates (Annual Percentage Yield or APY) compared to typical business checking or even basic savings accounts. This means that your business's idle cash isn't just sitting stagnant; it's actively working to grow your capital. These rates can be particularly appealing in a favorable interest rate environment, providing a noticeable boost to your bottom line without taking on significant risk.

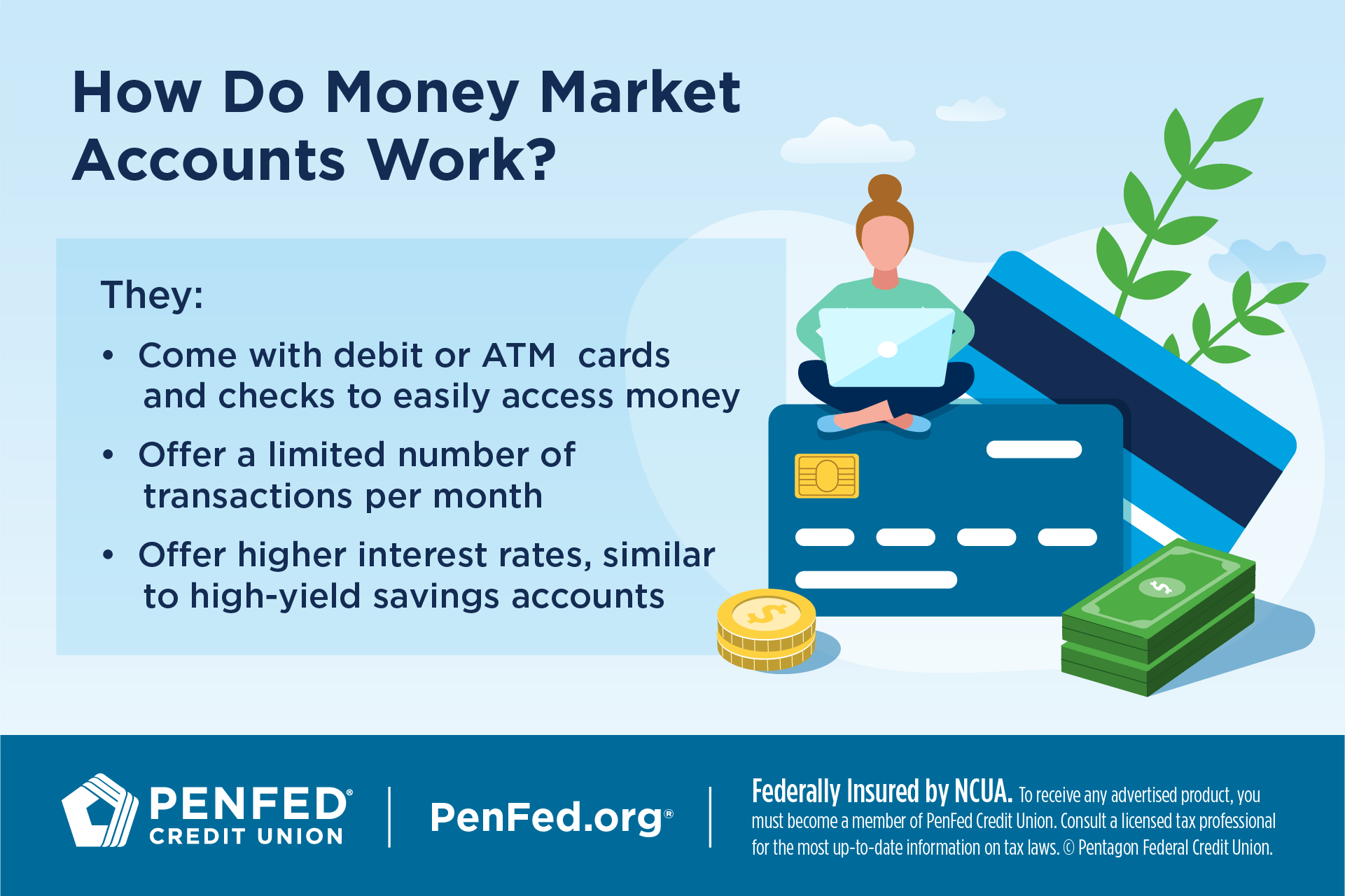

Enhanced Liquidity and Accessibility

Unlike Certificates of Deposit (CDs), which lock in funds for a fixed term, BMMAs offer superior liquidity. While they do have transactional limits (historically governed by Regulation D, which limited certain outgoing transfers and withdrawals to six per statement cycle, though this regulation has been suspended, institutions may still impose their own limits), they typically allow for check-writing privileges, ATM withdrawals, debit card access, and online transfers. This flexibility ensures that your business can access funds when needed for operational expenses, unexpected opportunities, or emergencies, without incurring penalties.

FDIC or NCUA Insurance: Peace of Mind

Security is a paramount concern for any business. Business Money Market Accounts offered by FDIC-insured banks or NCUA-insured credit unions provide federal deposit insurance coverage up to the maximum legal limit, currently $250,000 per depositor, per insured bank, for each account ownership category. This insurance protects your business's deposits even if the financial institution fails, offering a critical layer of safety and peace of mind for your valuable cash reserves.

Flexibility for Diverse Business Needs

BMMAs are versatile tools. They can serve as an excellent repository for short-term operational cash, seasonal income, or funds earmarked for upcoming tax payments. Their blend of earning potential and accessibility makes them a flexible option for various business cash management strategies, allowing you to react quickly to market changes or business demands.

How Business Money Market Accounts Operate

Understanding the mechanics of a BMMA is crucial for maximizing its benefits:

- Minimum Balance Requirements: Many BMMAs come with minimum opening deposit and ongoing balance requirements. Failing to meet these can result in lower interest rates or monthly service fees. High-yield BMMAs often have higher minimums.

- Tiered Interest Rates: It's common for BMMAs to offer tiered interest rates, meaning the APY increases as your account balance grows. Businesses with larger cash reserves can therefore benefit from incrementally higher returns.

- Transaction Limitations: Although Regulation D is suspended, financial institutions typically set their own limits on the number of outgoing transactions (e.g., checks, online transfers, debit card purchases) allowed per statement cycle without incurring fees. It’s important to clarify these limits with your chosen bank.

- Fees: Be aware of potential fees, including monthly maintenance fees (which can often be waived by maintaining a minimum balance), excess transaction fees, and overdraft fees.

Who Should Consider a Business Money Market Account?

A Business Money Market Account is particularly well-suited for:

- Businesses with Substantial Cash Reserves: Companies that regularly hold a significant amount of cash not immediately required for daily operations can benefit from the higher interest earnings.

- Organizations Seeking Better Returns on Short-Term Funds: If your business has funds designated for short-term goals (e.g., equipment purchase in 6-12 months, quarterly tax payments) and wants to earn more than a standard savings account without locking funds away in a CD.

- Businesses Prioritizing Liquidity and Security: Those that need quick access to their money but also value the safety of FDIC/NCUA insurance and a modest return.

- Seasonal Businesses: Companies with fluctuating cash flows can use BMMAs to store surplus funds during peak seasons, earning interest until the capital is needed during leaner periods.

Business Money Market Accounts vs. Other Business Accounts

To make an informed decision, it's helpful to compare BMMAs with other common business banking products:

Business Money Market Account vs. Business Savings Account

While similar in their interest-earning nature, BMMAs often provide slightly higher interest rates and more transactional flexibility (like check-writing) than standard business savings accounts. Both are typically FDIC/NCUA insured and have transaction limits, but BMMAs are designed for a slightly more active cash management approach.

Business Money Market Account vs. Business Checking Account

Business checking accounts are designed for frequent transactions and day-to-day operational needs. They offer maximum liquidity and usually have unlimited transactions but typically earn little to no interest. BMMAs, conversely, prioritize interest earnings and have limited transactions, making them unsuitable for primary operating funds but excellent for reserves.

Business Money Market Account vs. Certificate of Deposit (CD)

CDs generally offer the highest fixed interest rates among low-risk options but require you to lock in your funds for a specific term, with penalties for early withdrawal. BMMAs provide lower rates than CDs but offer much greater flexibility and liquidity, making them suitable for funds that might be needed before a CD matures.

Business Money Market Account vs. Money Market Fund (MMF)

This is a crucial distinction. A Business Money Market Account (BMMA) is a bank deposit account and is FDIC/NCUA insured. A Money Market Fund (MMF) is an investment fund offered by brokerage firms. While MMFs also aim for stability and generally invest in highly liquid, short-term securities, they are *not* FDIC/NCUA insured. Instead, they are typically protected by SIPC (Securities Investor Protection Corporation) up to certain limits for securities, but not against market value fluctuations. MMFs can offer slightly higher yields but carry a small, albeit low, risk of "breaking the buck" (where the net asset value falls below $1 per share), which is not a concern with FDIC-insured BMMAs.

Factors to Consider When Choosing a Business Money Market Account

Selecting the best BMMA for your business requires careful evaluation:

- Annual Percentage Yield (APY): Compare rates across different institutions. Look for competitive tiered rates if your business holds varying balances. Be mindful that rates are variable and can change with market conditions.

- Minimum Balance Requirements: Can your business comfortably meet and maintain the minimum balance to avoid fees and qualify for the best rates?

- Fees: Scrutinize all potential fees, including monthly maintenance fees (which can often be waived by maintaining a minimum balance), excessive transaction fees, and overdraft fees. Understand how to waive these fees.

- Transaction Limits: While flexibility is a benefit, ensure the transaction limits align with your business's anticipated need for accessing these reserve funds.

- Accessibility: Consider how easily you can access your funds – online banking, mobile app, branch network, and ATM access.

- Customer Service: A responsive and knowledgeable customer service team can be invaluable for business banking needs.

- Bank Reputation: Choose a reputable financial institution with a strong track record and good financial health.

Current Trends and Outlook for Business Money Market Accounts

Recent news indicates that money market accounts, including business-specific ones, have seen competitive interest rates. However, the economic landscape is always shifting. Financial publications often highlight the "best money market accounts" based on current APYs, emphasizing the importance of businesses continually shopping around for optimal rates. There has also been discussion about whether the era of "fabulous money market rates" is nearing its end, suggesting that while rates have been strong, businesses should be aware of potential future changes. The comparison between high-yield savings accounts and money market accounts remains a recurring theme, with businesses encouraged to understand the subtle differences to choose the most suitable option for their cash management strategies. The emphasis remains on balancing attractive yields with necessary liquidity and, above all, the security of FDIC/NCUA insurance.

Conclusion

A Business Money Market Account can be a powerful tool for businesses seeking to maximize their idle cash while maintaining crucial liquidity and security. By offering competitive interest rates, FDIC/NCUA insurance, and a degree of transactional flexibility, BMMAs provide a sophisticated solution for managing short-term reserves. Understanding their features, comparing them with other financial products, and carefully evaluating different offerings will enable your business to make an informed decision and foster stronger financial health. Don't let your business's cash reserves sit stagnant; empower them to grow with a strategically chosen Business Money Market Account.